Your credit union or community bank is constantly chasing younger demographics – Gen Zers, Millennials and growing families. And you’re right to do so if you want to grow loan volume.

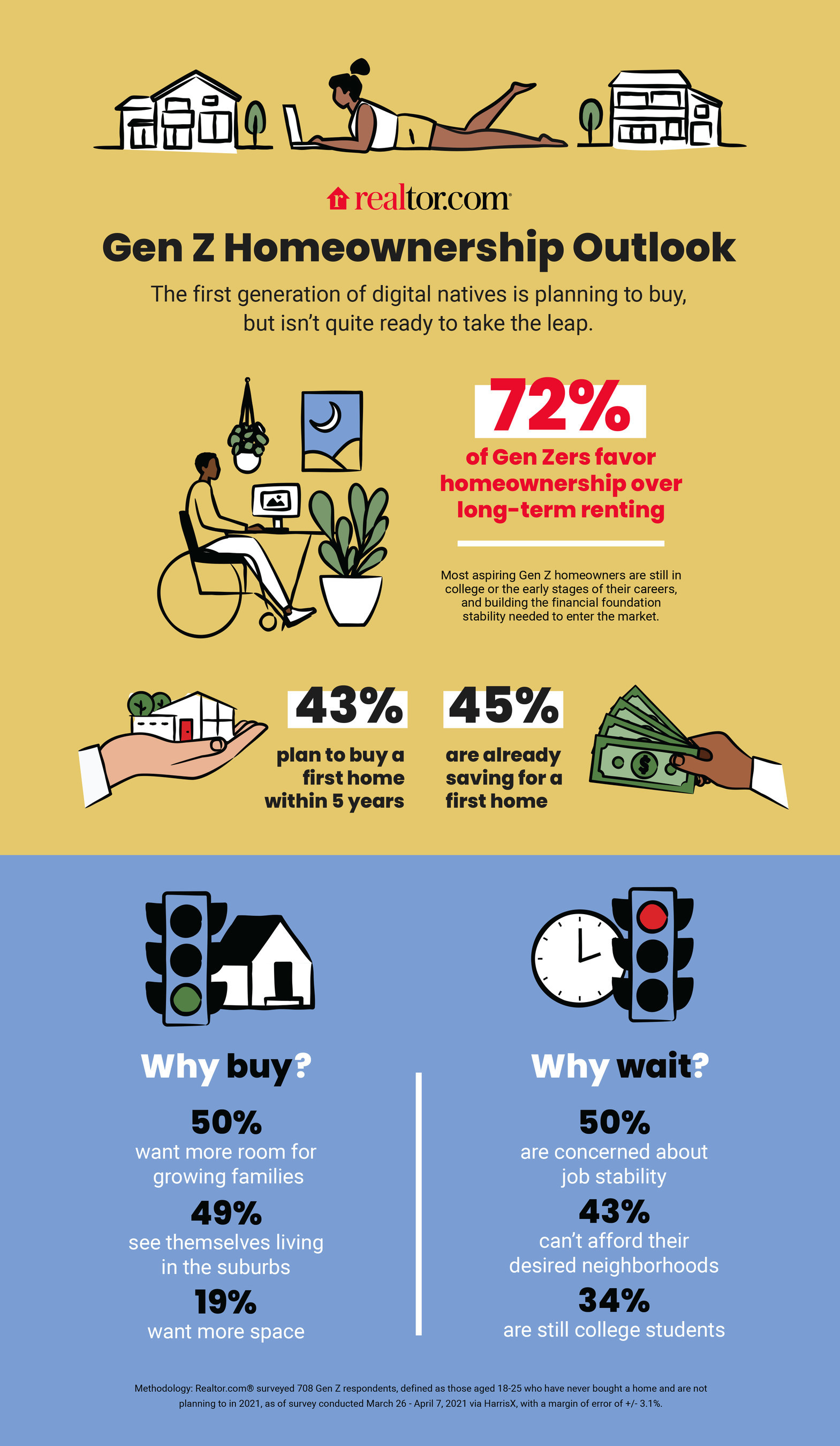

Data shows 44.6% of Gen Z wants to own a home in the next five years, and Millennials make up 43% of all 2022 homebuyers. If you’re after a strong mortgage program, it’s impossible to ignore these groups.

But what do younger demographics want from lenders? How do you get them to choose you over someone else?

Maybe I can provide some insight. My wife and I are on the older end of Gen Z (who were born between 1997 to 2012), and we just bought our first house. We were lucky enough to have a lender we loved. She was kind, knowledgeable and made the process as easy as possible.

Here are four things our lender did to appeal to us as Gen Z home buyers.

1. She Made Pre-Approval Convenient

When it comes to younger demographics, convenience is key. Just look at the data. Physical branch visits frustrate 75% of Gen Zers, and convenient online banking is important to 90% of Millennials.

Physical visits would have frustrated us too. My wife is a teacher, so it’s near impossible for her to take off work for a lending appointment. And even if it was after work, that’s one extra thing to do after a long day.

Our lender made sure we never visited a physical location. She completed every stage of our pre-approval either over phone or email, giving us the convenient experience we craved.

2. She Helped Us Resolve Credit Score Snags

During the pre-approval process, we found out my wife didn’t have a credit score. “Oh no! It’s game over,” we thought. But our lender didn’t see it that way. She immediately hatched a plan to generate a credit score for my wife.

We followed the lender’s plan to the letter. Within two months, my wife had a credit score (and a good one too).

There are some situations where the answer is “no.” Not everyone’s ready to buy a house. But if it’s a solvable issue, help the buyer solve it.

Like my wife, a lot of young people don’t have credit scores or don’t know how to build credit. In fact, 45 million American adults have no score. This is a solvable issue. Don’t let a little elbow grease get between a buyer and their dream home.

3. She Responded Quickly to Estimate Requests

Responsiveness is essential in today’s market.

Our home was on the market for one day. We put an offer in the day we saw it, so we needed quick estimates to double check its affordability. There was no time to slow walk the estimates, and thankfully, our lender didn’t.

Rapid response times give buyers confidence in their offer, and they give realtors confidence you’ll close the deal on time. Don’t give buyers or realtors reason to worry about your dependability.

4. She Went Above and Beyond What Was Necessary

All the nitty-gritty loan details mean nothing if you’re not making human connections with buyers.

At our closing, the lender showed up and gave us a candle for the new home. There’s no requirement to do either of those things, but she did them anyway. She went above and beyond to show she cared about us.

If you go back to the beginning of this post, you’ll notice I said we “loved” our lender. That’s pure emotion. We loved our lender, so we wanted to tell everyone about her. Buyers will do the same thing for you if you go above and beyond what is necessary.

If you tried these methods and still aren’t seeing increased loan volume, there may be bigger issues sabotaging you. On The Mark Strategies offers consumer experience training to take your interactions with members or customers to the next level. Book a free consultation today!

{kind=link}